The Problem With Passive Indexing

But also why we may not have any other choice...

Welcome back, everyone! I hope you all had a fantastic week!

This week we want to be a bit controversial. After all, it is pretty fun to be controversial sometimes is it not?

But in actuality, we really are after some thought-provoking ideas that undermine the general sentiment about investing, particularly passive investing. It can be good to shake up the status quo a little bit every now and then.

So what specifically are we targeting?

Index Funds

Nearly everyone knows what an index fund is (if you’re involved with investing communities), essentially they are a “basket” of stocks that provide diversification while keeping your expenses low and your investments simple.

And so far, stock performances are also on the side of index funds with over 100 years of data proving the simple premise that “stonks go up.”

But even with that considered, I do think there are some downsides to index funds and the indexing community. So, in no particular order, here they are.

It Overvalues The Whole Market Regardless of Fundamentals

You may have heard of “the index fund bubble.” A possible scenario in which the existence (and dominance) of index funds pushes the prices of stocks up above where they would reasonably be valued at. Essentially the aspect of price discovery is eliminated in the markets via the majority of investors simply not looking at stock fundamentals.

Obviously, this is not good for price efficiency. But how does this matter to the individual investor?

Well, first of all, a bubble eventually pops and it usually isn’t pretty. But what’s more concerning is the possibility of poor future stock market performance. A few posts back we looked at the impact of an asset bubble on Japan’s stock market. This ultimately has resulted in low single-digit returns for several decades.

This topic has received a lot of attention in recent years especially considering the transition from active to passive investing has sped up exponentially.

Even the Atlantic covered it in their article titled “Could Index Funds Be ‘Worse Than Marxism’?”

And as you can see these fund inflows have a correlation with the CAPE ratio (an inflation-adjusted PE ratio).

This can be very concerning for new investors that have not had the opportunity to purchase stock at low multiples since from a business standpoint, it takes much longer to achieve their ROI.

Long Periods of Flat/No Growth in The Stock Market

This is something we’ve talked about before. Even though stocks in the long term have a general uptrend, over shorter time frames that is not the case. And I’m not talking about just a year or two, I mean over decade-long periods.

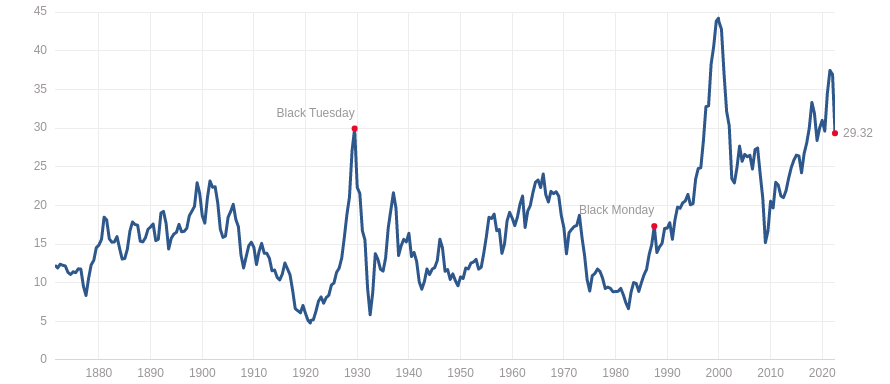

Just take a look at this chart:

Over the last 120 years, there have been four separate periods where real returns were 0% for over a decade.

Considering that time is one of the biggest assets of an index investor, this is really concerning.

If an investor were unfortunate enough to even lose ten years off of portfolio growth at a 10% annual return over a forty-year career it would halve their portfolio value.

For those in the Financial Independence Retire Early (FIRE) community, this could be even worse considering they are often looking to retire in their 30s or 40s. This gives their portfolio about 20-30 years max before they need to use it for withdrawals in retirement.

Again, if you look at the chart, there are three whole periods where real stock market returns were 0% for nearly two decades.

However, the fact that investors have a fairly high likelihood of experiencing a zero real return decade over their investing career is not what I am trying to get at specifically.

The problem is that this is not really discussed in investing communities. No one ever talks about the possible decades of no growth your portfolio might experience because over the long term “stonks go up.”

For people barely getting into the space, there should be more done to make them aware that this is part of the process. I believe that the bull market of the last ten or so years made people forget it is possible for the stock market to stagnate for long periods of time, and that isn’t really healthy for new and relatively inexperienced investors’ confidence.

Your Net Worth Is Capped At Around 5 Million For The Average Person

Now immediately you might be thinking, five million? That’s more than enough money for anything!

And you’re right. It is a lot of money, about $170,000 after capital gains tax based on the 4% rule.

But still, it does not change the fact that there is a cap. Your portfolio size is almost completely dependent upon your annual income.

In order to reach a five million dollar portfolio size in twenty years (a fairly normal FIRE time frame) you would need to contribute $90,000 every year. That’s more than the average household income in the US being invested into an index fund each and every year.

Without earning an enormous salary, there is nearly zero chance that your net worth will be able to break this five million barrier. That is the trade-off made for having a more secure and predictable method of retirement.

If you are the kind of person that intends to be part of the very high net worth or ultra-high net worth club, you will need an alternate method to index funds.

Most likely, you’ll have to do much of the grunt work of starting or buying businesses yourself. That’s exactly the same way Warren Buffett was able to amass his fortune, as well as many other multi-millionaires and billionaires.

Indexing Is NOT Actually Passive

This point is not necessarily a disadvantage, but I think it’s important to point out that indexing is not as passive as most people think.

If you take a close look at the S&P 500 or the Dow Jones Industrial Average indexes you might notice something peculiar.

A study conducted in 2004 even shows that if the additions and deletions to the S&P 500 had not been performed over the years the annual percentage return would actually be higher.

The study breaks the strategies employed into three separate categories.

The survivor’s portfolio consists of only shares from the original companies in the S&P 500. Any spin-offs or mergers are immediately sold to reinvest in the original companies.

The Direct descendant’s portfolio consists of survivors plus shares issued by a firm acquiring an original S&P 500.

And lastly, the total descendant portfolio consists of all original companies plus any mergers or spinoffs from those original companies.

As you can see, all three of these portfolios were able to outperform the standard S&P 500 with its changing components every year.

Essentially, the index underperformed itself!

But what about total market funds? There’s no strategy to those! Those are completely passive!

Not so fast, even these funds have to make a fundamental decision over how to allocate their portfolio. Oftentimes funds are “cap-weighted” as in, they are included in the portfolio as a percentage of the company’s total value. This is opposed to equal weight or inversely weighted portfolios.

The point is that certain decisions are made about these portfolios which makes them not completely passive. At the end of the day, if you are trying to beat the market, you are just trying to beat index fund managers in how they allocate their index funds! Not some mystical market forces that combine into complete knowledge efficiency…

The market is a bit of an illusion when you think of it this way.

If you’re interested in further related content, I found this other newsletter that also tackled the issue with index funds, albeit, in a different direction.

To Conclude…

Maybe this rant is a bit hypocritical since the majority of my holdings also happen to be index funds. But, I’m willing to recognize that they are not the magic bullet that many investors make them out to be as they do have their own issues. But... they still may be one of the best options we have (aside from value investing).

Anyway, if you found this article interesting or learned something new, please take a moment to share or subscribe to this newsletter. It’s completely free, and I don’t spam your inbox with promotional content, so you can be assured you don’t have to be deleting garbage emails every day.

Just hit that green button!

With that said…

Until Next Time!

All content is for discussion, entertainment, and illustrative purposes only and should not be construed as professional financial advice, solicitation, or recommendation to buy or sell any securities, notwithstanding anything stated.

There are risks associated with investing in securities. Loss of principal is possible. Some high-risk investments may use leverage, which could accentuate losses. Foreign investing involves special risks, including a greater volatility and political, economic and currency risks and differences in accounting methods. Past performance is not a predictor of future investment performance.

Should you need such advice, consult a licensed financial advisor, legal advisor, or tax advisor.

All views expressed are personal opinion and are subject to change without responsibility to update views. No guarantee is given regarding the accuracy of information on this post

Great article! New investors tend to conflate index and passive investing, but hidden turnover can be quite substantial, as you point out. I previously wrote about these kinds of problems over here: https://www.svegroup.com/education/limitations-of-passive-investing

I'd love to get your thoughts on selling shareholder voting rights as a way to generate passive income. At SVE (https://svegroup.com), we're building the first exchange for buying and selling shareholder votes. Let me know what you think!

> Your Net Worth Is Capped At Around 5 Million For The Average Person

Question 1: Is it possible that the average passive indexer is not part of the mean (since it is more middle class ish)? https://ifstudies.org/blog/can-intelligence-predict-income https://pumpkinperson.com/2014/11/09/hypocrites-who-deny-linear-iq-income-correlation/

Question 2: Does the amount of funds available affect peak returns (e.g. leverage, risk tolerance)?