Revisiting The Best Market Beating Strategy

+16% Annualized Returns For Three Decades, I'm not joking...

Welcome back everyone to this weeks edition of Premium Income Investments! This week I want to revisit something we spoke about several months ago. Namely leveraged index investing.

This strategy has always been controversial and especially so during the market downturn we have experienced this year.

Personally I am down a little over 30% with my leveraged funds (hedgefundie portfolio) to date.

And on the Bogleheads reddit forum…

No doubt this has been probably the scariest time for this strategy with a massive drawdown smacking every proponent of it in the face. But this is not something that we were unaware of.

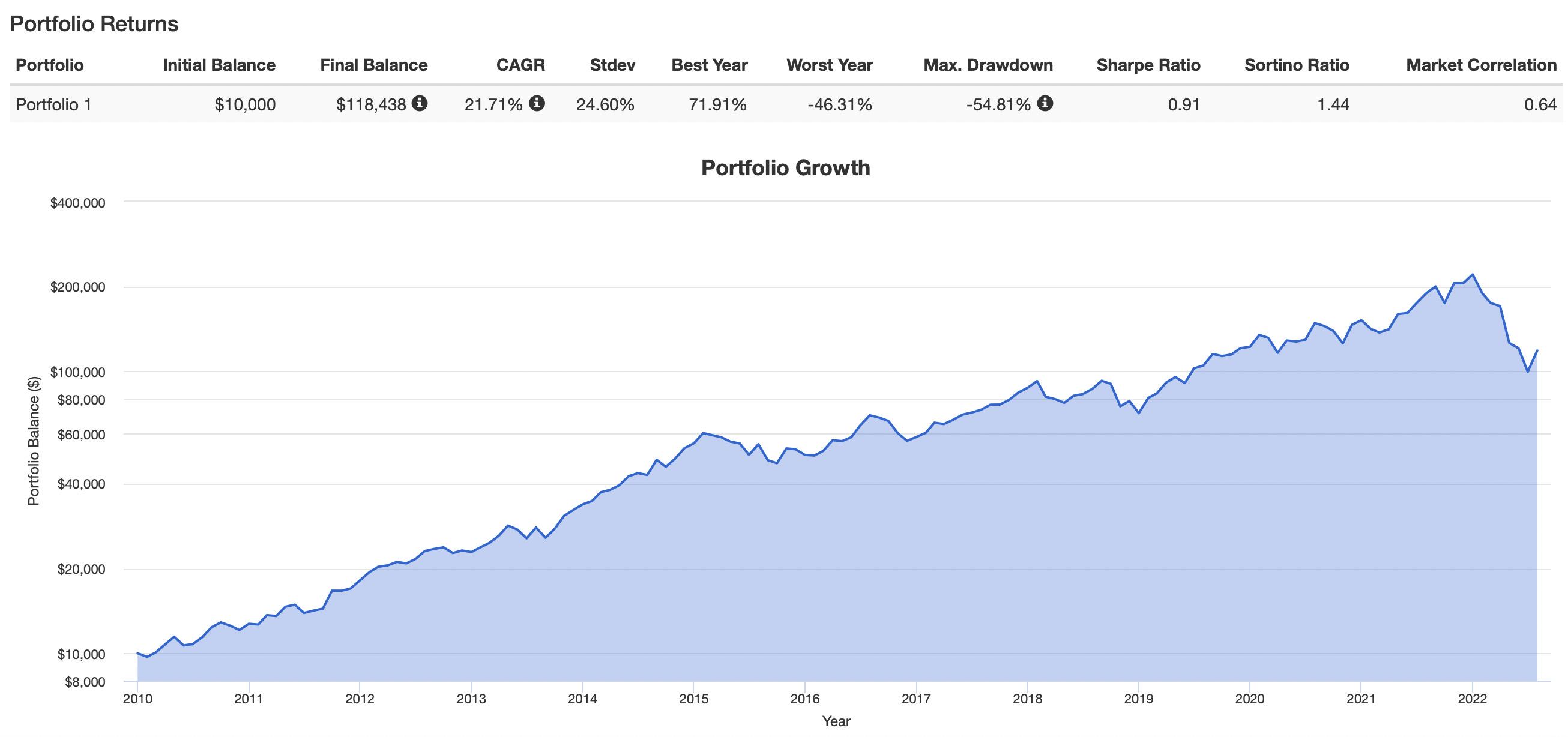

The backtests very clearly show that large drawdowns are to be expected. Even in the raging bull market of the last decade or so there was still an entire year that the portfolio was down 46.31%! That’s the inherent tradeoff with the strategy, you cannot expect a 20% annualized return without a wild ride of volatility.

Often times when this strategy is discussed there is no middle ground. People either hate it and believe it will never work long term, or they are so optimistic that when a large drawdown happens (like what’s happening right now) they become fearful and sell for a loss. As always, I think its important to look at things from both sides so we can get a complete picture of whether it would make a good investment for you as an individual.

Pros:

16% annualized returns since 1987. The difference this makes is astounding, $100k would be worth over $8M compared to $1.7M with a 10% annualized return.

It’s simple, the funds themselves are already managed for you, all you need to do is rebalance the portfolio once per quarter. (Typically I do a 55% UPRO 45% TMF split because that’s what Hedgefundie used)

Lots of exposure and diversification. These funds are the same as a S&P 500 fund and Long term treasury fund except with extra leverage. It is well known that an equities and bond portfolio increase Sharpe ratio by reducing volatility. We attempt the same thing but with leverage.

Cons:

Big drawdowns and high volatility. This is the nature of leveraged products. The Sharpe ratio is still high, but only because the returns increase along with the volatility of the portfolio.

The underlying funds could go broke. Because of the 3x leverage employed with these funds, all that would need to happen to bankrupt them is a 33% loss in a single day. This is highly unlikely and there are protections (i.e. circuit breakers) in place to stop it from happening, but hindsight is 20/20. No one ever thought it would be possible for Enron and WorldCom to go out of business like they did, but it happened regardless. With regular index funds there will still always be something left because all of the largest companies in the US would have to fail at once. (if that happened you have bigger problems than how much money you have for retirement).

The portfolio assumes equities and bonds have a negative correlation, that is to say, if equities got wiped out bonds would save the portfolio and vice versa. Historically this has been true, but as we all know, the past is not always an indicator of the future. Most recently we have seen the equities and bonds correlation go positive due to rising interest rates.

So… what kind of investor profile is suited for this kind of portfolio then?

After all, hedgefundie himself, the creator of the portfolio, considered it very risky and allocated only 10% of his net worth into it even though he was in his early 30s.

Here’s my take on the ideal candidate for this strategy:

Young with 20-30 years until retirement minimum. Ideally the latest you would want to start investing like this would be in your 30s.

High risk tolerance. A person capable of taking a 50-60% maybe even 70% loss without considering selling or panicking. You really need to trust the data with this strategy, otherwise there is no way you will hold long term enough for it to work.

Competent about investments. You should at least be familiar and invested into some index funds and understand that “Mr. Market” can be wildly unpredictable at times. Ideally you should be familiar with all the drawbacks and potential flaws with this strategy before investing in it.

If leveraged indexing sounds like something you would be comfortable doing I would highly recommend reading this thread by Hedgefundie before investing a dime.

It’s also something to note, at the annualized return that the Hedgefundie portfolio provides it does not take a lot of money to make a lot of money.

For example, if you were invest $10k at age 30, by the time you turn 60 you should have over eight hundred thousand dollars…

This assumes that you make no other investments…

If you happened to be well positioned financially by thirty years old, you could do even better. One hundred thousand dollars could become eight and a half million!

Again, if your risk tolerance is not high enough, or you believe that you are too close to retirement, this most likely doesn’t apply to you. This kind of investment can be like a lottery ticket to your primary investments. Your primary investments will carry you through just fine if it doesn’t pan out, but if it does? Well, that’s the icing on the cake.

Some Closing Thoughts For Today…

Before I end this article I want to share something I stumbled across while writing this piece that I found pretty interesting. I might write an article on it in the future, but if you’re interested here’s a link. It’s a strategy about “buying the dip.” According to the backtests it beats buy and hold by a significant margin. The person who came up with it said they have been doing it for several years with good results. I won’t make any opinion on it now, but I think its definitely worth looking into.

Anyway, if you liked this article please subscribe! It really helps me out. I’ve also added a referral tool that tracks your referrals and allows me to give you cool stuff! I’ll probably be making some kind of limited referral merch soon so stay tuned! You can click the button below to get started!

All content is for discussion, entertainment, and illustrative purposes only and should not be construed as professional financial advice, solicitation, or recommendation to buy or sell any securities, notwithstanding anything stated.

There are risks associated with investing in securities. Loss of principal is possible. Some high-risk investments may use leverage, which could accentuate losses. Foreign investing involves special risks, including a greater volatility and political, economic and currency risks and differences in accounting methods. Past performance is not a predictor of future investment performance.

Should you need such advice, consult a licensed financial advisor, legal advisor, or tax advisor.

All views expressed are personal opinion and are subject to change without responsibility to update views. No guarantee is given regarding the accuracy of information on this post