Pushing The Boundaries of Efficient Frontiers

Finding outliers... Or a Ponzi scheme

In Our Last Article We Discussed The Importance of The Efficient Frontier

But in this article we want to expand on an idea:

The efficient frontier will always have the “sideways parabola” look to it. However, the exact curvature of it can shift based on the assets and strategies we are using.

The shift in the curvature is where we find our alpha to beat the market, and here’s how we can do it.

By adjusting our asset allocation or our strategy we can shift this frontier. In fact we can even show the frontier difference between a small selection of stocks.

Here we have the efficient frontier of five stocks, CNP, F, WMT, GE, and TSLA.

And here we have tickers AAPL, GM, AAL, CCL, and A.

As You Can See, Asset Allocation Makes a Huge Difference On The Efficient Frontier.

In the first curve we see a more linear correlation between returns and volatility. At 20% returns we have roughly a 22% standard deviation, 25% returns has a 25% standard deviation, and 30% returns has a 30% standard deviation. However the second curve skews much higher on the standard deviation side. A 20% return has a 27% standard deviation and a 25% return gives a 32% standard deviation.

However, we are not constrained to simply play within the boundaries of the efficient frontier. While a combination of assets can be used to generate an efficient frontier by differing the weights, a “strategy” does not work in the same way. This is simply because the strategy determines not only what asset combinations are used, but also the assets themselves will change on a regular basis. So when constructing a strategy, we do not develop an efficient frontier around it, it only represents a single point to which we can compare to an already existing efficient frontier.

With a good strategy in determining our stock selection, we can change our Sharpe Ratio, hopefully putting us outside the efficient frontier.

Building A Strategy Outside The Benchmark Frontier

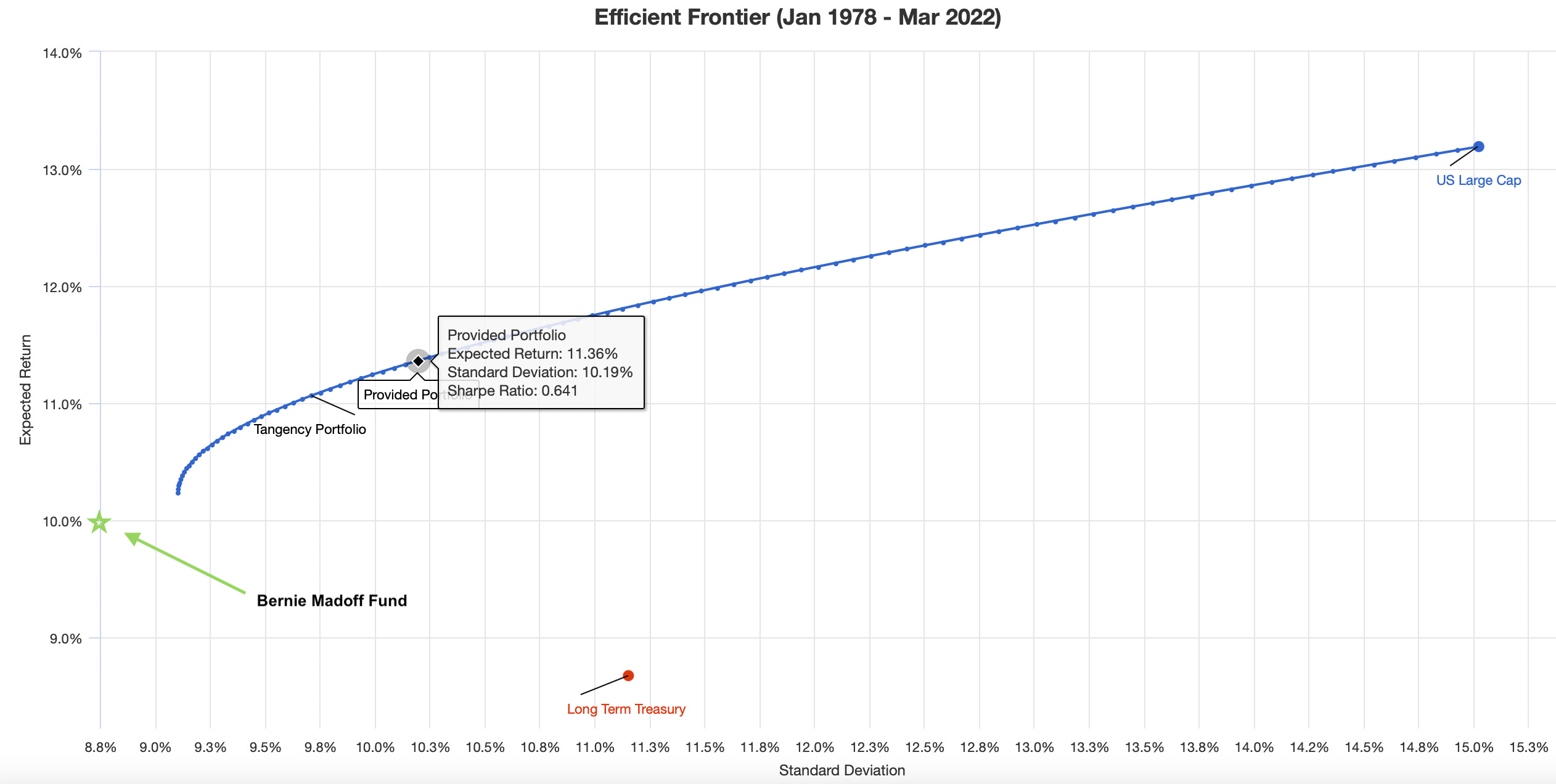

This picture shows the frontier for a US Large cap and long term treasury mix, which if you ask most any investor this is what the benchmark frontier should look like.

Our goal is to create a point that pushes this boundary using some type of semi-active strategy.

We know that this is possible because of two reasons:

Warren Buffett has consistently beat the Sharpe ratio of the market and this frontier using traditional value investing

The S&P 500 itself is a semi-active strategy

And now you might be thinking, the S&P 500 is not a semi-active strategy, its completely passive. Invest it and forget it.

You would be right too, but only for yourself. Every year professionals construct what is added or removed from the index, it is not simply static. So the question is, what exactly gets added and removed and how do they determine it?

Well, the S&P 500 is fairly simple, it consists of large cap industry leaders. So a company that has fallen out of favor or no longer remains an industry leader will be removed with up and coming stars being entered in.

So we know that its possible to beat this frontier (because it has been done) and the idea of this frontier being “ideal” or “the standard” is faulty because it is a semi-active strategy itself. If we simply build rules as if we were creating our own index in the same way that the S&P 500 index is built on rules we can beat the market and fall outside the efficient frontier by simply constructing “better rules.” If you think about it, this is exactly what Warren Buffett has done, he has constructed his own “index” that operates on consistently defined rules to determine what stays in the portfolio and what leaves.

That’s great and all, but how do we go about creating our own “index”?

That’s what our investment prowess is for! Find correlations between higher returns and some other trait and you have a winning strategy.

However, here are some ideas that could be worth exploring as we create our own “indexes.”

The effect of liquidity on returns. Perhaps stocks with low liquidity are more likely to have mispricings that we can take advantage of to pump up our returns.

The effect of diversification on returns. Do we really need 500 stocks or more to be truly “diversified”? Our goal should be to achieve max diversification to return tradeoff. Too much diversification and we dilute our winners, too little and we have wild swings of volatility.

The effect of weighting on returns. Which types of portfolio weighting methods are associated with higher returns? Equal weight? Cap weight? Inverse cap weight? Some other weighting method?

Ponzi Scheme On The Efficient Frontier

Just for fun, we’ll look at what a Ponzi scheme looks like when compared to our efficient frontier like we said we would last time.

Bernie Madoff ran his scheme from 1960 to 2008 with an average 10% return. This itself is not the surprising part. The surprising part, was that the annual volatility of the fund was 2.45% according to this paper.

If we compare it to the stock/bond frontier from earlier his fund would be further left then the chart can even show!

In fact, his Sharpe ratio ranged anywhere from a whopping 2.5 to 4.0!

That alone should had said volumes about the shady things that were going on inside the fund.

So why exactly does this have any importance to us now?

Well, simply put, if you want to figure out if a fund hinges on a Ponzi scheme all you need is the standard deviation and average return. If when you plot that on a graph it falls significantly (and I mean significantly) outside the curve shown for stocks and bonds, you should be VERY skeptical.

Anyway, that’s all for today! Until next time!

If you love our newsletter, why not share it? We’re sure someone else will love it too!

We’ll even make it easy for you with this big green button!

Disclaimer:

All content is for discussion, entertainment, and illustrative purposes only and should not be construed as professional financial advice, solicitation, or recommendation to buy or sell any securities, notwithstanding anything stated.

There are risks associated with investing in securities. Loss of principal is possible. Some high-risk investments may use leverage, which could accentuate losses. Foreign investing involves special risks, including a greater volatility and political, economic and currency risks and differences in accounting methods. Past performance is not a predictor of future investment performance.

Should you need such advice, consult a licensed financial advisor, legal advisor, or tax advisor.

All views expressed are personal opinion and are subject to change without responsibility to update views. No guarantee is given regarding the accuracy of information on this post

Question: can a Logarithmic Curve or Square Root Curve be used to detect and eliminate Ponzi schemes (Efficient Frontier has a clear shape)?