Mutual Funds vs Indexing

Do Mutual Funds Really Suck as Much as Most People Think?

Nearly Everybody Knows That Passive Indexing Outperforms Mutual Funds or Active Investing

Chances are you’ve heard the statement, “95% of actively managed funds failed to outperform the market over the last 20 years.” Maybe the percentage is not always the same, but it is always a very high number that underperform the market.

Today, we want to dive into this debate and beyond just the surface statistics. This statement is promulgated so much that it has become the end all be all in most investing circles without any further research being done to see how “true” this statement and its implications actually are.

The Quote Comes From This Report:

Every year since 2002 the SPIVA active vs passive report card has shown that passive investing generally outperforms active investing.

Depending on the funds you compare it to, they underperform anywhere from 78.95% of the time to 99.71% of the time. This is quite significant, but remember, this is over 20 years. So at least a fraction of these funds have proven that they can outperform. Out of the fraction of funds that do outperform, maybe it’s possible that it is not just random, but that there are funds that consistently outperform due to good management and strategy.

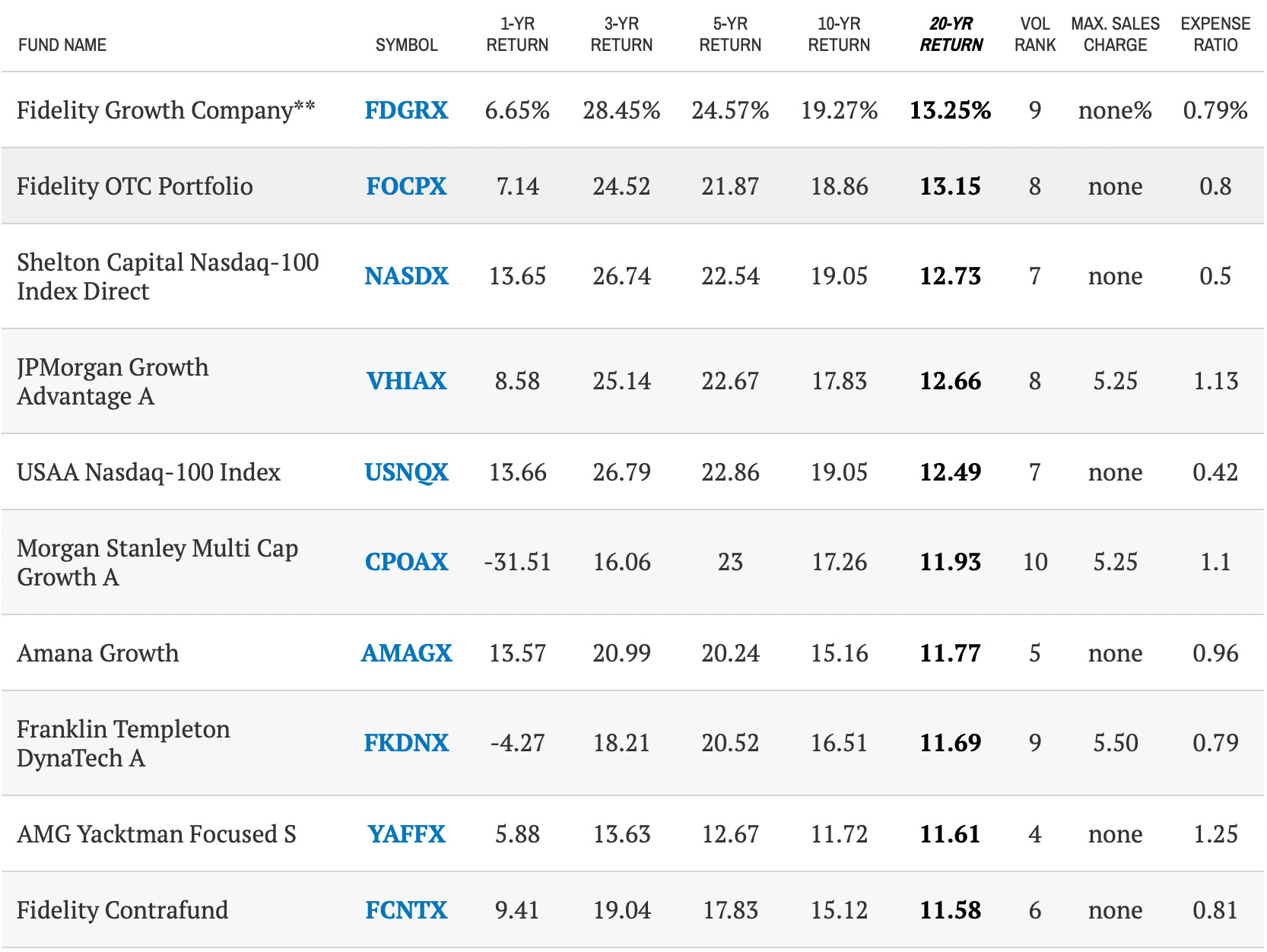

If We Visit Kiplinger We Can Find a List Of These Funds That Have Outperformed

According to portfoliovisualizer.com SPY has returned an average CAGR of 9.09% non-inflation adjusted since January of 2002 (ending in March of 2022). So as we can see all of these funds beat the overall market over the last twenty years by at least two percent.

And just in case you’re wondering how significant a two percent change in returns is, it correlates to roughly 2x over forty years.

This is a very significant change! Which makes me think that our investigation into mutual funds is not in vain.

So let’s compare the second fund, FOCPX against VFINX in portfolio visualizer.

FOCPX over the course of 37 years from inception has beat the market by a significant margin. However, this image does not really show the whole picture.

Why you may ask?

Because it does not account for headwinds or tailwinds in the equities market. You see, even though we know the market returns 10% on average, that average is taken over a decades-long time frame. As you begin to approach 40-50 years your returns will smooth out, but up until that point they can be highly dependent on prevailing market conditions.

As you can see throughout history there have been long periods of no real returns in the stock market as well as periods where the market 10x’d in only a decade or two. When comparing an index fund against a mutual fund this should be something that we account for, as the when we invest is about as important as the what we invest in.

Anyone can cherry-pick data and make an investment appear to perform better than it actually does, but we’re not trying to cherry-pick data, we’re trying to look at the investment from different angles so we can see all of its possible merits and drawbacks.

In the case of FOCPX, we’re looking at it decade by decade as well as during bull markets and markets with zero returns to give a more complete picture.

1985 - 1990 FOCPX outperformed the index (15.66% CAGR) by 3.84% a year not only in total returns, but also risk-adjusted. (Sharpe: 0.61 to 0.52)

1990 - 2000 FOCPX outperformed the index (15.3% CAGR) by 1.91% a year, although not on a risk-adjusted basis.

2000 - 2010 FOCPX underperformed the index (0.32% CAGR) by 0.4% a year leaving you with a non-inflation adjusted negative return.

2010 - 2020 FOCPX outperformed the index (13.83% CAGR) by 5.71% a year on a risk-adjusted basis. (Sharpe 1.05 to 0.96)

For the 1985 - 2000 Bull market FOCPX outperformed the index (16.72% CAGR) by 2.89% a year, although surprisingly not on a risk-adjusted basis.

For the 2000 - 2013 Flat market FOCPX underperformed the index on a total return basis by 0.83% a year (1.53% CAGR for the index) although when adjusting for the risk, it outperformed.

(And remember that these returns account for the expense ratio of FOCPX)

Over most periods (predominantly bull markets) FOCPX has proved capable of beating the index. The time where it struggles against the index were chiefly bear/stagflation environments.

Intuitively, this makes complete sense when we take a look at how the fund categorizes itself. Large Growth is quite responsive to extended bull markets but tends to get hammered during bear markets. Its current asset allocation puts it at over 46% in the tech sector.

Most periods of time also happen to be dominated by bull markets, in fact, according to this article the market hits an all-time high on average, sixteen times a year. That comes out to be an all-time high every 22.8 days!

With this being the case, it is no wonder that FOCPX performs well.

So What About The Other Funds? How Do They Perform?

Well as we mentioned before, this is highly dependent on not just what the funds invest in, but also when you invest in them.

This idea takes me back to the book by James O’Shaughnessy What Works On Wall Street. At the beginning of the book, he talks about how consistency is the real key when it comes to investing. When we change strategies every five minutes we never really know what actually works, because strategies often work over years and decades rather than days or months. A particular investing strategy may underperform over a specified period, but that doesn’t make it a bad investment per se.

Mutual funds, just like index funds are vulnerable to the concept of sequence of return risk, even during the growth period and not just the retirement period of an investor’s life. As the chart above would indicate, investing in an index fund could have zero returns over a long period if you invest at the wrong time.

One of the most legendary investors of all time, Warren Buffett has had periods where he underperformed the general indexes, but that doesn’t make him a bad investor. On the contrary, we look at his entire performance over the years and conclude that he can accurately pick stocks and outperform the market averages.

I think this should be the same light that we view mutual funds or other constructed portfolios. To say that because a fund underperformed for a few years makes it a bad investment is short-sighted.

To overcome this we simply need to look at the funds from different angles to get the most complete picture of how effective they are (or not effective they are) over different time periods and market conditions. When we more accurately see the risk profile of a fund or portfolio we can stick with it even when it seems to underperform.

So again, how did the other funds perform?

Well, since inception, all of them except one (VHIAX) outperformed the market. Five of the ten funds failed to beat the market on a risk-adjusted basis, (even though they managed to beat it on a total return basis) these include FKDNX, CPOAX, USNQX, VHIAX, and NASDX.

(In the case of lower risk-adjusted returns, it simply means that if we used leverage to up the returns of our index fund we could get to the same level of risk but with more returns. Obviously, this is not ideal because if we can get better returns with the same level of risk, why bother investing in a mutual fund? If you want to read more about this you can check out this other article we wrote about leveraged index funds.)

To continue though, we see that FDGRX beat the market over each of the four decades (not quite four but almost) while only losing to the index on a risk-adjusted (but not total return) basis for one decade. Even over the lost decade, FDGRX managed to beat the overall market on a risk-adjusted and total return basis.

FOCPX did not fare near as well, however, it did beat the market over three of the four decades since its inception on a risk-adjusted basis. The fund did not beat the market over the lost decade either.

AMAGX was the next fund that beat the market (risk-adjusted) since its inception. It was created in 1995 and over the three decades (roughly) that the fund has been in existence, it has beaten the index risk-adjusted for all of them. Surprisingly, this actually includes the lost decade. AMAGX managed to beat the index on a risk-adjusted basis by over 3% a year during this period.

YAFFX is one of the newer funds which makes it a bit less trustworthy than the others (inception date 1997) but for the two and a half decades in its existence, it managed to beat the index for two whole decades on a risk-adjusted basis. (2017 until now has not been too kind to the fund as it underperformed the index’s CAGR of 16% by about 2.5% a year) The crazy thing about this fund is that it INSANELY outperformed the index over the lost decade. In fact, if you had looked at this fund alone you might assume that there never actually was a lost decade. From 2000 to 2010 this fund managed an 11.82% CAGR compared to the index’s 0.32% on a risk-adjusted basis.

Last up we have FCNTX, which over the four decades since its inception (1985) has not failed to outperform the market on a risk-adjusted basis over any of them, including the lost decade. Its returns over the lost decade aren’t quite as impressive as YAFFX, however, it did still manage to outperform by about 4% a year.

So Should We Consider Mutual Funds As A Viable Investment?

Based on the data I would say we can safely say that they are a viable investment. However, the question of whether there are other good investment alternatives out there? There definitely are. Mutual funds are by no means perfect, but the main point of this article was to dispel the myth that seems to be common in indexing circles that mutual funds are as good as worthless.

Typically mutual funds are attacked from several angles:

They have high expense ratios. This is by far one of the most common arguments. In today’s world, anything above the 0.05-0.1% expense ratio is considered expensive and not worth investing in. And this does have merit if the fund you invest in only ever underperforms. Not only do you lose out to the market, but you have to pay more for doing so.

They oftentimes underperform the market. This is the other really common argument against mutual funds, which according to the SPIVA report is completely accurate. As you could see, only half of the funds on the list from Kiplinger even beat the market since inception on a risk-adjusted basis.

It’s simpler to invest in the total market, which is completely valid. But if you want to simplify your investments and not think about them, why are you reading this in the first place? And why do these people participate in investing forums? With the time they spend writing and reading investment news and keeping up with current markets they might as well direct their energy into finding out-performers. Again this point is highly dependent on an individual’s personality, some people enjoy looking for investments and others do not.

Past performance of a mutual fund is no indicator of future returns. This statement gets said all the time, specifically by index fund advocates. This assertion, like many of the others, is also correct. Past data can never 100% predict future returns, if it did, everybody would be millionaires off of the stock market. Now given that, at the same time, past performance is one of the best indicators of future returns that we have. After all, what else besides past data can we use to predict future returns? (Even company fundamental data is considered “past” data.) However, one thing that I’ve noticed consistently is that index fund advocates like to say this and follow it up with the performance of the indexes over the past century as proof of why they are safe/good investments. I have nothing against them, and even own index funds myself, but it does seem a bit hypocritical.

Management changes from time to time. This is not really something I accounted for in this analysis, but if you decide to take a shot at analyzing mutual funds yourself, then this should definitely play a factor in your pick. If a superstar mutual fund manager leaves, it’s possible that the superstar mutual fund performance will as well.

Lastly, mutual funds with the best performances are usually closed to new investors. This is not really a surprising revelation considering what the implications of running an open fund are for the managers. If an open mutual fund outperforms over a series of years, investors will be more likely to want to invest in it to get a slice of the action. The problem is that when a fund expands rapidly like this, the fund manager has to deploy this capital somehow or risk underperforming. However, if they deploy the capital into their already existing holdings, they go more concentrated than would be ideal. This rapid expansion of capital for deployment is possibly the cause that kills its outperformance that made it attractive in the first place. In our example from above, we see one of the best funds of the group, FDGRX, as being a closed fund. If an investor can get access to one of these funds by either being gifted shares thus allowing them to purchase more or being offered them through a retirement plan, it might be wise to investigate its performance and possibly purchase it.

There are a lot more aspects of mutual funds that could be touched on of their pros and cons, but hopefully, this article has convinced you that mutual funds are not the devil that they have been made out to be. Do your research and it is possible to find good funds, and like all strategies, it should not make up 100% of your portfolio else you risk underperformance during a bad period.

Anyway, if you liked this article or it opened up your mind to some new aspect of investing please take a moment to share it with someone. It could be your mom, your cousin, or heck, even that nephew that is way too much into crypto (or maybe that’s you, we’re not gonna judge). Sharing this article would really help us to deliver more quality content to you and it only takes a couple of seconds. We’ll even put this green button here to make it easy.

And if you want to get more content like this consider subscribing to our newsletter! We send out one per week and they’re all free, you don’t have to worry about us spamming your inbox. Just make sure to add our email to your email contacts so our letters don’t go to your spam folder.

With that said…

Until Next Time!

Disclaimer:

All content is for discussion, entertainment, and illustrative purposes only and should not be construed as professional financial advice, solicitation, or recommendation to buy or sell any securities, notwithstanding anything stated.

There are risks associated with investing in securities. Loss of principal is possible. Some high-risk investments may use leverage, which could accentuate losses. Foreign investing involves special risks, including a greater volatility and political, economic and currency risks and differences in accounting methods. Past performance is not a predictor of future investment performance.

Should you need such advice, consult a licensed financial advisor, legal advisor, or tax advisor.

All views expressed are personal opinion and are subject to change without responsibility to update views. No guarantee is given regarding the accuracy of information on this post

Secondary question: what are the percentage of mutual funds that can consistently beat index funds in 10-year windows post-fees? How about those that are index funds masquerading as mutual funds (matching performance)?