Learning From Warren Buffett

Berkshire Hathaway 1979 Analysis

Welcome back, everyone!

We hope you have not been looking at your portfolio too much with the bloodbath currently going on.

But, even if you have been watching it every minute and biting your fingernails we have some good news, stocks are going on sale!

Our old friend Warren Buffett has taken advantage of the recent market turbulence to establish over fifty billion in new positions. We hope you’ll follow in his footsteps and do the same.

Several weeks ago we wrote about Warren Buffett’s 1977 annual shareholder letter. Some key ideas we saw pop up, were the importance of valuation when purchasing a business, managerial competence, and enduring profitability.

Today we are going to analyze the 1979 shareholder letter to see if we can find any other interesting data. (I’m passing over the 1978 letter because it mainly focuses on the performance of Berkshire’s various investments as opposed to investing strategy.)

But before we get too deep into the mud, we’ll look at the context of the time period to get a more complete picture of Buffett’s advice.

Some Context…

1979 saw some familiar things to what we are seeing right now. Inflation was at an all-time high of 11.25%.

And the federal funds rate hovered anywhere from 10-16% throughout the year.

And the economy was right on the cusp of a recession… not great times for business or investing…

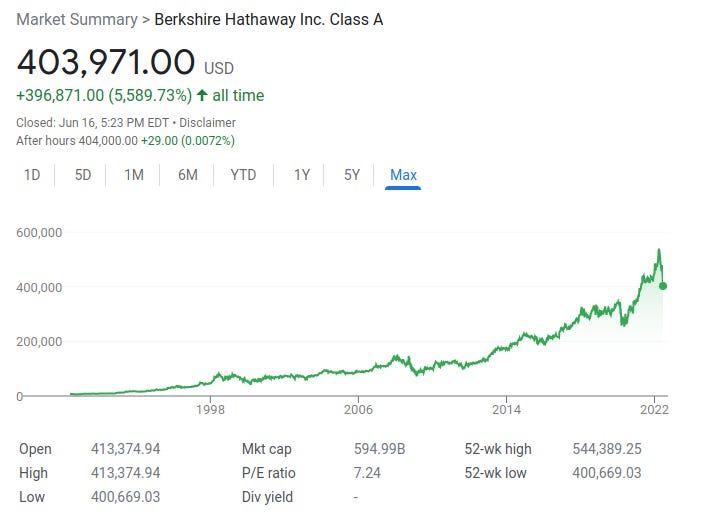

Berkshire for nearly a decade had stagnated, however, going from 1979 to the early 1980s we see Berkshire rocketing up several hundred percent.

Today those class A shares are worth nearly half a million dollars.

So with that information clearly in view, let’s take a dive into the letter.

The link to the 1979 letter is here.

The letter opens by talking about some changes in accounting practices that determine how securities owned by insurance companies are displayed on the balance sheet. This made the insurance companies owned by Berkshire look much more attractive than they were in actuality according to Buffett.

Beyond that, though Warren still feels confident in their performance as a company and states:

We have achieved this result while utilizing a low amount of leverage (both financial leverage measured by debt to equity, and operating leverage measured by premium volume to capital funds of our insurance business), and also without significant issuance or repurchase of shares. Basically, we have worked with the capital with which we started.

This is a noteworthy statement because when you analyze the figures on Berkshire it turns out that Warren has been using a leverage ratio of approximately 1.6:1. To a lot of people, this may come as a surprise considering that Warren advocates for no leverage and investing in an S&P 500 index for most people.

In order to achieve this leverage ratio, Buffett uses insurance float.

What is insurance float?

Insurance float is the reserve of money that insurance companies keep from collecting premiums that have not been paid out in claims yet. If you ever sold an option contract before, it is very similar to what insurance companies do.

You sell the option for a profit but take the risk that the stock will move unfavorably for you.

This pleasant activity typically carries with it a downside: The premiums that an insurer takes in usually do not cover the losses and expenses it eventually must pay. That leaves it running an “underwriting loss,” which is the cost of float.

Instead of making money from collecting premiums, insurance companies turn around and invest the premiums in order to earn a profit before they need to pay out claims. The cost of “borrowing” this money from the policyholders is called the cost of insurance float. (It’s also possible that a company makes money on their insurance float, but that is not the case for Buffett.)

For Buffett, his cost of insurance float was estimated at 2.2% in 2013.

Considering that we just came off of near zero-level interest rates, that may not be very impressive but keep in mind, that this is a long-term average.

Buffett has been able to borrow money for this cheap for decades…

The other benefit to this kind of borrowing for him is that he cannot get a margin call on this debt. So even if the market value of Buffett’s securities falls significantly it will not make him insolvent like it would with a retail investor.

Warren is able to turn around and used this cheaply borrowed money to buy high-quality cheap stocks which are commonly known as value investing.

This begs the question “what kind of returns could be achieved with leveraged value investing in a retail portfolio?” It might be something interesting to ponder for your portfolio.

We already know that a leveraged ETF portfolio has consistently beat the market for nearly four decades so why can’t we do that with value investing?

Moving On…

Warren follows up his discussion of the microeconomic factors of the business with a more macro-level picture of the current economic condition. As we already mentioned, it wasn’t very good.

If we should continue to achieve a 20% compounded gain - not an easy or certain result by any means - and this gain is translated into a corresponding increase in the market value of Berkshire Hathaway stock as it has been over the last fifteen years, your after-tax purchasing power gain is likely to be very close to zero at a 14% inflation rate. Most of the remaining six percentage points will go for income tax any time you wish to convert your twenty percentage points of nominal annual gain into cash.

Without getting political, it is a bit obscene what the government does in situations like this. They inflate the money supply and then they tax as they normally do, essentially a double tax on your investment income.

There is not really a clear-cut best way to avoid a situation like this, the best we can do is stay invested, and don’t sell our assets. One could argue that something like inflation-protected bonds like TIPS could be bought to ensure no loss of capital, but in order to not lose money, you must hold the bond until maturity. If you don’t, you are subject to the whims of the secondary bond market with wild price fluctuations.

And if you hold it until maturity, you might end up holding it through a stock market recovery, in which case you would have been better off staying invested anyway…

Warren sums up all this thinking here:

That combination - the inflation rate plus the percentage of capital that must be paid by the owner to transfer into his own pocket the annual earnings achieved by the business (i.e., ordinary income tax on dividends and capital gains tax on retained earnings) - can be thought of as an “investor’s misery index”. When this index exceeds the rate of return earned on equity by the business, the investor’s purchasing power (real capital) shrinks even though he consumes nothing at all. We have no corporate solution to this problem; high inflation rates will not help us earn higher rates of return on equity.

Lastly, Buffett Discusses A Bank That They Acquired:

This will be the last year that we can report on the Illinois National Bank and Trust Company as a subsidiary of Berkshire Hathaway. Therefore, it is particularly pleasant to report that, under Gene Abegg’s and Pete Jeffrey’s management, the bank broke all previous records and earned approximately 2.3% on average assets last year, a level again over three times that achieved by the average major bank, and more than double that of banks regarded as outstanding. The record is simply extraordinary, and the shareholders of Berkshire Hathaway owe a standing ovation to Gene Abegg for the performance this year and every year since our purchase in 1969.

This seems to be time-specific knowledge that’s not very relevant upon first look, but after reading this second part I would say it illustrates a good point.

As you know, the Bank Holding Company Act of 1969 requires that we divest the bank by December 31, 1980. For some years we have expected to comply by effecting a spin-off during 1980. However, the Federal Reserve Board has taken the firm position that if the bank is spun off, no officer or director of Berkshire Hathaway can be an officer or director of the spun-off bank or bank holding company, even in a case such as ours in which one individual would own over 40% of both companies.

Warren essentially said the bank that they owned was a spectacular investment, and yet according to this Bank Holding Company Act, they were forced to sell it. This is not a good situation for Buffett, however, whoever acquired that bank after Buffett would have made a spectacular investment.

This is a perfect example of market inefficiency that an investor could take advantage of. There are opportunities like this in the stock market as well, with one great example being the Hedgefundie portfolio.

Obviously, the purchase of large businesses like this is a low liquidity level market which makes market inefficiencies more common, but that doesn’t mean that there aren’t any in the stock market or other highly liquid markets.

Let’s keep our eyes open and continue looking for opportunities…

By the way, if you enjoyed this article, please consider subscribing and sharing it with a friend! It really helps us out. And if you have any questions or comments don’t hesitate to drop them below, I’ll be sure to respond to all of them.

Until Next Time!

Disclaimer:

All content is for discussion, entertainment, and illustrative purposes only and should not be construed as professional financial advice, solicitation, or recommendation to buy or sell any securities, notwithstanding anything stated.

There are risks associated with investing in securities. Loss of principal is possible. Some high-risk investments may use leverage, which could accentuate losses. Foreign investing involves special risks, including a greater volatility and political, economic and currency risks and differences in accounting methods. Past performance is not a predictor of future investment performance.

Should you need such advice, consult a licensed financial advisor, legal advisor, or tax advisor.

All views expressed are personal opinion and are subject to change without responsibility to update views. No guarantee is given regarding the accuracy of information on this post.