Berkshire Hathaway Annual Letter Analysis

Things to learn from Buffett himself

This Week We’re Going to Be Doing Something A Little Different

In the past we focused on strategies that could help us beat the market. However, today we’re going to take one from Warren Buffett’s playbook and read through his 1977 shareholder letter to see if there is anything in it to help us generate some alpha. Warren Buffett has been known to provide good information in all of his shareholders that is not just applicable to his company, but to security analysis in general. The greatest part about this? You can read all of them for free online!

But First Some Context…

The 1977 Berkshire Hathaway shareholder letter is the first publicly available letter on Berkshire’s website. You can find them all at this website. 1977 was the first good year that Berkshire had in eight years. According to this post Berkshire had a annualized -2.6% return from 1968 to 1976, this was despite a book value increase of 647% during the period. However, at the beginning of 1980 the share price had rocketed up from $38 in 1976 to $290. At this point in time Buffett was running a company that was severely undervalued that the market simply refused to realize its value. This is also part of the reason the phrase “the market can stay irrational longer than you can stay solvent” exists. Eight years that this investment stagnated even when it was growing significantly.

Now Into The Letter

Buffett opens by talking about what defines managerial competence. He says that simply increasing earnings year over year is not impressive by itself. As “even a totally dormant savings account will produce steadily rising interest earnings each year because of compounding.” Instead he believes that “Return on Equity Capital” otherwise known as Return on Equity (ROE) shows the competence of the managers as it demonstrates how efficiently they deploy their capital and resources.

This is something noteworthy worth exploring. Can looking for stocks with high ROE alone have good returns when compared to the overall market? According to this backtest conducted in Backtesting-Based Value Investing the answer is a resounding yes!

The backtests conducted were from the period of 2001 to 2013 during which the broad market had a total return of 42.31%, one of the flattest decades since the 60s and 70s.

(See image for reference)

That’s a CAGR of only 2.75%! However, when we turn to the ROE portfolio, we see a massive outperformance with a 7.96% CAGR. The construction of this portfolio is simple, it consists of 20 of the highest five year average ROE stocks in the S&P 500 with rebalances occurring annually. In fact, if we throw in in a low price to book ratio as well the returns jump to a 9.34% CAGR.

Now granted, this is only a thirteen year period, but it is significant that this occurred during one of the worst performing decades in history.

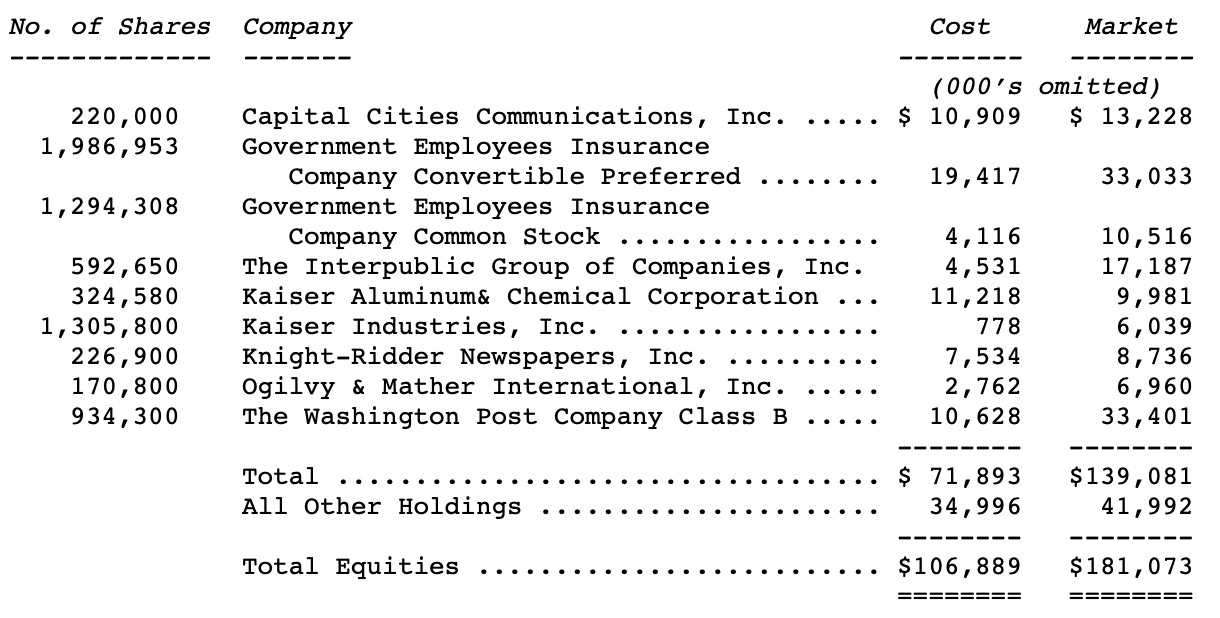

Following this Warren talks about the specifics of some of the companies in his portfolio and how they have been performing. He then goes into the equity holdings of the insurance companies underneath Berkshire Hathaway which look as follows.

Not surprisingly, Warren states that the criteria he uses to buy marketable securities hardly differs from the criteria used to acquire a company as a whole.

His criteria are as follows:

The business needs to be one that can be understood by the investor.

The company must have favorable long term prospects.

The company must be operated by “honest” and “competent” people.

The business must be purchasable at a “very attractive price.”

The first criteria is one that is often overlooked. We think we know what a company “does” but that is not always the case. A great example of this is McDonald’s. McDonald’s on the surface appears to be a fast food company, but dig a little deeper and you will realize that they are actually in the real estate business and rather, it is the franchisees who are in the fast food business. According to Wall Street Survivor “In 2014, the McDonald’s corporation made $27.4 billion in revenues, of which fully $9.2 billion came from franchised locations and the rest ($18.2 billion) was from company-operated restaurants” and “McDonald’s keeps close to 82% of all their franchise-generated revenue versus only 16% of its company-operated restaurant revenue.”

Favorable long term prospects are one of the harder things to quantify or understand, especially in an industry like tech where everything is constantly changing. For Buffett, this has meant sticking to to businesses that have proven long term prospects like Coca Cola, Apple, and Bank of America.

The third criteria of competent management is also highly important. One need look no further than Berkshire Hathaway itself. Much of its performance over the decades can be attributed to Warren Buffett’s and Charlie Munger’s investing prowess and being able to find good value companies. Prior to their acquisition of the company it was largely unknown.

Finally the last criteria is where we see a large influence by Benjamin Graham. A “very attractive price” usually constitutes a company that is trade very close to or possibly even below its book value. In today’s market this is much harder to come by with the ease of credit and record high CAPE ratio. However, this should not be taken that value investing has fallen out of favor entirely, but simply that it is going through an unfavorable cycle. When the next market crash occurs many companies will return to more reasonable valuations.

Another Concept Worth Paying Attention To:

We select our marketable equity securities in much the same way we would evaluate a business for acquisition in its entirety. - Warren Buffett

The key thing we should be concerned about is the mindset shift when we consider acquiring the company as a whole. It detaches our view of the stock market from “a line that goes up or down that can make or cost me significant sums of money” to investing in concrete businesses.

Let’s take a step back and look at private equity deals for a minute for comparison.

In the case of private equity with businesses valued under $5 million they trade hands at a 3-5x EBITDA multiple. In public markets EBITDA is far higher due to the size and stability of the company (closer to a 15x EBITDA). This valuation multiple is highly important to investors because if the multiple is too high then there will be no money to cover the debt service that is usually incurred in the leveraged buyout (up to 90% of the value is usually borrowed). On top of this, it also usually means that investors in private equity at these valuation multiples expect high returns (approximately a 25% CAGR according to HBR’s Guide to Buying a Small Business) in order to make it worth their while with low liquidity and higher risk.

The point in comparing our investments to the way that private equity runs theirs is that we should be chasing the same things. Even if our public investments don’t pay their earnings out in dividends we should act as though they did when choosing them. The moment we stop doing this we fall prey to buying companies at poor valuations.

I believe this is the heart of what Warren Buffett is trying to communicate here in regards to public equity markets.

Anyway…

This was definitely a different type of newsletter compared to what we normally do. However, we think that even though it did not place quite the same amount of focus on quantitative investing principles as we usually do there is still valuable things to learn. If you found this article interesting please help us out by clicking that green share button! We promise it will only take you a couple seconds to send to someone else that may enjoy it.

If you have any questions or comments feel free to drop them below! We will be responding to all!

Until Next Time!

Disclaimer:

All content is for discussion, entertainment, and illustrative purposes only and should not be construed as professional financial advice, solicitation, or recommendation to buy or sell any securities, notwithstanding anything stated.

There are risks associated with investing in securities. Loss of principal is possible. Some high-risk investments may use leverage, which could accentuate losses. Foreign investing involves special risks, including a greater volatility and political, economic and currency risks and differences in accounting methods. Past performance is not a predictor of future investment performance.

Should you need such advice, consult a licensed financial advisor, legal advisor, or tax advisor.

All views expressed are personal opinion and are subject to change without responsibility to update views. No guarantee is given regarding the accuracy of information on this post